Light Weight And Strong Woven Nylon Insulated Safety Rope

Used for guide and ground wire traction, instead of anti-twist wire rope.It has the characteristics of light weight, good insulation and high strength, and the price is different from that of denimar traction rope, which can effectively reduce the loss of self.

Woven Nylon Insulated Safety Rope be widely used:Fire rescue, outdoor climbing, outdoor rock climbing, fire fighting training, high-altitude operation, high-altitude construction, etc.

Woven Nylon Insulated Safety Rope details:

Woven Nylon Insulated Safety Rope specifications:

Model

Nominal Diameter

Line density(g/m)

break load(KN)

HJS-4

4

13

3.1

HJS-6

6

20

5.4

HJS-8

8

44

8.0

HJS-10

10

64

11.0

HJS-12

12

93

15.0

HJS-14

14

117

20.2

HJS-16

16

157

26.0

HJS-18

18

193

32.0

HJS-20

20

222

38.0

HJS-22

22

268

48

HJS-24

24

318

52

Safety Rope,Woven Safety Rope,Nylon Safety Rope,High-Altitude Work Safety Rope Hebei Long Zhuo Trade Co., Ltd. , https://www.hblongzhuo.com

Did the strong recovery in August signal the overall upward trend in the auto market? Is the impact of the continuous deterioration of Sino-Japanese relations on Japanese cars contagious? Can independent brands make progress later and reverse the trend? Will the dealer's inventory pressure in the fourth quarter be reduced with the peak sales season? Around these issues, Gasgoo.com launched the latest phase of the industry survey (from September 17 to September 23, 2012, the number of participants is 1023). The following will be combined with the expert's interview one by one.

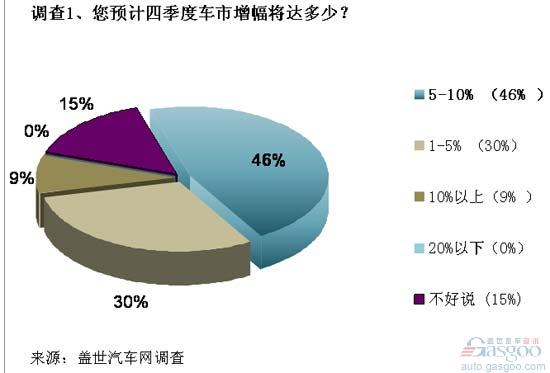

According to the results of Survey 1, people in the industry are optimistic about the increase in the auto market in the fourth quarter. Nearly half of the participants believe that the growth will continue the trend in August, and the growth rate is expected to reach 5-10%, the highest proportion of this group of people is 46%; Second, about 30% of people are cautious about the trend of the auto market in the fourth quarter. Optimistic attitude, that the increase will not be higher than 5%. Others believe that the growth rate of the auto market in the fourth quarter may exceed 10%, but this proportion only accounts for 9% of the total number of voters.

Since “Jin 9 Silver 10†and the year-end consumption boom are both located in the last quarter, this quarter is the traditional peak season in the Chinese consumer market. Auto consumption is the largest consumer activity in China in addition to real estate consumption. It will also usher in this period. Traditional sales peak. At the same time, automakers will also introduce a number of preferential sales policies in order to complete the established annual sales target. In the first half of this year, most of the transcripts submitted by car companies are not optimistic. Out of the 24 major passenger car companies in China, only three companies have completed half of the sales target for the whole year, and the "internal test" has a ratio of only 1/8. Therefore, the auto market competition before the end of this year is bound to become more intense, and the sales promotion of the auto market is expected to be even greater than in previous years.

Some of the more cautious people think that the auto market in the fourth quarter is not much better than last year. Expectations of a sluggish economy next year, and high oil prices will delay purchases; congestion will increase the risk of urban extensions, and the decline in Japanese car sales caused by the deterioration of Sino-Japanese relations may affect terminal sales growth. This group of people believe that the positive growth of the auto market in the fourth quarter is already a good ending. The number of people holding such a cautious attitude is not a minority, accounting for as high as 30% in our survey. They think that the increase of the auto market in the fourth quarter should be between 1-5%.

There are 15% of the participants taking a wait-and-see attitude, that the constraints of multiple factors are still not clear, the auto market growth in the fourth quarter is still not clear judgment, chose "not to speak." However, before comparing the previous two quarters of the auto market expectation survey, we believe that the industry’s confidence in the overall performance of the Chinese auto market in the fourth quarter is significantly stronger than the previous negative growth and slight growth (less than 5%). ,

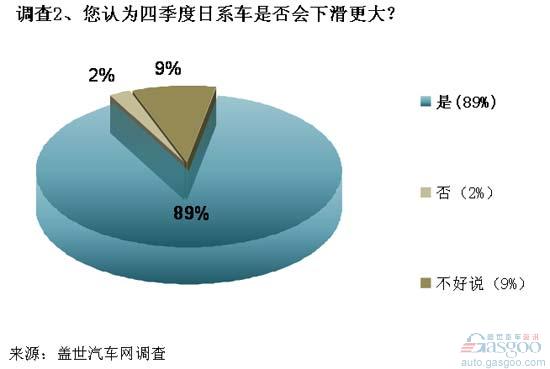

In Survey 2, we focused on the future performance of Japanese cars in the industry, and whether Japanese car sales will decline in the fourth quarter. The results showed that as many as 89% of the participants believe that the further political antagonism between China and Japan will inevitably deepen the difficult situation of Japanese cars in China. Japanese cars will face a greater decline in sales in the future.

The dispute over the sovereignty of the Diaoyu Islands, which has been selectively shelved, began to escalate in July after Japan’s right-wing forces staged a farce on the island’s island. The boycott of Japanese goods that broke out in multiple cities in August has recently swept the country. From the current public data, the sales of the six Japanese automakers entering the Chinese market in August in the terminal market have confirmed the impact of the current situation. Toyota's and Mitsubishi's four Japanese automakers experienced different degrees of decline from the same period last year. Nissan Motors, which had previously maintained a two-digit high growth rate for five consecutive months, only increased by 0.6% in August. In addition to the higher growth of Honda vehicles due to the promotion of low-price strategy and new car sales such as CRV, the overall performance of Japanese cars in August was poor.

In September, the tension between China and Japan was once again escalated, and the incidents involving the Japanese cars that appeared in many places undoubtedly affected the decision of potential consumers of Japanese cars. They either delayed purchases or chose other brand cars. Before and after 9.18, Japanese car manufacturers were forced to stop production, and their marketing and promotion activities were also forced to stop. In light of the fact that the situation in China and Japan is unlikely to be solved in the short term, the decline in Japanese cars in the fourth quarter or even longer will be difficult to avoid.

In addition, some experts believe that Japanese cars are not favored. Apart from the consumer boycott caused by the tension between China and Japan, the lack of competitiveness of Japanese auto companies is also a factor that cannot be ignored. At present, Japanese cars have encountered strong offensives in Europe and the United States in the mid-to-high end market, and ethnic groups have resisted in the middle and low end. The improvement in this situation is not overnight.

In survey 2, only 2% of participants believe that Japanese cars will not decline in the fourth quarter. Another 9% of participants considered it difficult to judge and chose not to speak.

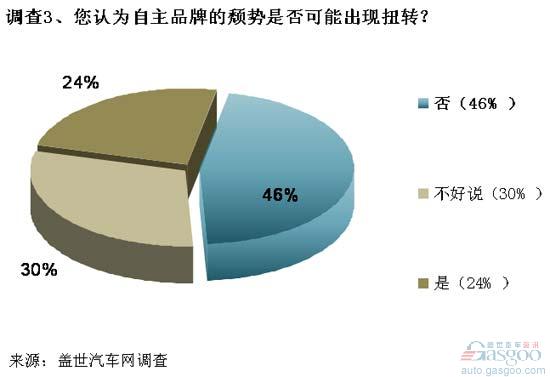

The possibility that the self-owned brands have been able to reverse in the fourth quarter of this year is still small. In survey 3, we sought the opinions of people in the industry on this issue and found that 46% of participants believe that their own brands will not stop falling in the fourth quarter.

Dong Yang, secretary-general of the China Automobile Association, pointed out that the market share of self-owned brands in the first eight months was in a downward trend, and this decline will continue in September and October, and no situation can be reversed. According to the latest sales data released by the China Automotive Industry Association, the market share of self-owned brand passenger cars has continued to decline. In August, the sales of self-owned branded passenger vehicles accounted for 444,100 vehicles, accounting for 36.4% of the total passenger vehicle sales. The market share decreased by 0.3% from the previous month and decreased by 0.8% year-on-year. From January to August, 400.82 million self-owned brand passenger cars were sold, which accounted for 40.3% of the total sales of passenger cars. The market share decreased by 2.4 percentage points from the same period of last year. Among them, the sales of self-owned brand cars declined even more. From January to August, the sales of self-owned brand cars were 1.817 million, a decrease of 4.4% over the same period of the previous year, accounting for 26.4% of the total sales of cars. The occupancy rate was down by 3% from the same period of last year. .

According to historical data, the market share of self-owned brand passenger cars should have risen significantly in August compared with that in July, but this year it has continued to decline in August, and the production and operation pressure of self-owned brand passenger vehicles has been increasing. Recently, the Ministry of Industry and Information Technology and the leaders of development and reform have successively issued joint-venture autonomies. This further deepens the industry’s concerns about self-owned brands. Once the joint venture has been officially defined as an independent brand, it can be supported by the state at the policy level. This will undoubtedly be a heavy blow to the traditionally independent brand. Local brands that are already exhausted will respond to the foreign brand market in the future. While investigating, it is necessary to make every effort to guard against the encroachment of the joint venture's own brand, and its pressure will further increase in the future.

In addition, some participants believe that it is not easy to predict the fourth-quarter trend of independent brands in the current environment. The Chinese automobile market is a typical policy market. The national macroeconomic policy has a decisive influence on the direction of the market. It is impossible to know whether the national level will introduce a supportive policy for independent brands in the fourth quarter. Therefore, as many as 30% of the participants It is not easy to say that the trend of independent brands has been chosen. While the remaining 24% of participants believe that relying on the local version of the subsidies and the advent of the "second spring" of auto exports, the self-owned brand may reverse its downturn in the future.

Although in the short term there is no clear industrial policy to promote the support of independent brands at the national level, a number of local subsidy policies have already been introduced, such as subsidies for Changan Automobile in Chongqing, subsidies for FAW's own brands in Jilin Province, etc., although only some regions. Sexual subsidy policy, but it is bound to effectively boost sales of local self-owned brands in the coming period of time.

In addition, export support for the self-owned brand's capacity digestion and earnings support is already showing. According to the latest data on China's auto exports, China exported 487,900 vehicles in the first half of the year, an increase of 28% year-on-year. According to forecast, China's total auto export volume is expected to exceed one million units this year, and the year-on-year increase will reach 27.48%; the export volume is expected to reach US$17.472 billion, which is an increase of 59.37% compared with the same period of last year. Industry insiders generally believe that the domestic independent brand passenger car has ushered in the "second spring" of exports.

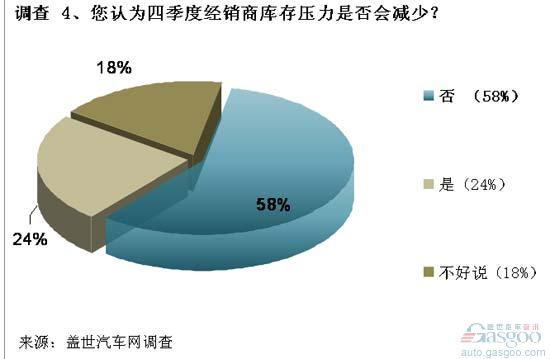

As some car enterprises have set excessively high annual growth targets at the beginning of the year, some car companies have begun to transfer inventory pressure to dealers, which has directly contributed to the long-term high inventory of some auto brands. In the fourth quarter, what kind of changes will happen to dealers’ stocks, and will the pressure be reduced as the market picks up? In our survey4, 24% of the participants gave a positive reply and believe that the dealership inventory pressure will slow down in the fourth quarter. However, more people hold objections and believe that the inventory pressure of dealers in the fourth quarter is still very large and will not decrease. This proportion accounts for 58%. Another 18% of participants chose not to speak.

According to the "Auto Dealer Inventory Survey Results" issued by the China Automobile Dealers Association, the inventory of automobile dealers increased significantly in the first half of the year. Inventories of automobile dealers continued to climb in June, and the comprehensive inventory coefficient reached 1.98. Of the 41 brands involved in the sample survey, 10 had an inventory coefficient of more than 2.5. In July, the dealer's inventory coefficient began to decline. The dealer's comprehensive inventory coefficient fell to 1.70, a decrease of 0.28 from June. Among them, the inventory coefficients of auto dealers of joint ventures, imports, and independent brands were 1.61, 1.77, and 2.04, respectively, and the overall level was still higher than the alert level of 1.5. According to Luo Lei, deputy secretary general of the China Automobile Dealers Association, dealer inventory pressure will continue to ease in August, but it will still be above the alert line of 1.5.

In order to complete the year-end target, auto manufacturers will step up efforts in the fourth quarter. This means that the manufacturer will press a large number of stores to the dealers. Once the dealers cannot keep up with the transaction volume, the pressure on the stocks may not drop or rise. Although the problem of manufacturers' press warehouses is often criticized, analysts believe that passenger car companies are the central pillar of steady local GDP growth. It is difficult for manufacturers to reduce their production, and most manufacturers cannot change the rhythm of production and sales due to complaints from dealers. However, in actual operations, manufacturers can increase the efforts to allocate promotional subsidies to dealers to help dealers deal with the shortage of funds caused by inventory. Luo Lei of the Auto Circulation Association also suggested that manufacturers should establish a rapid response mechanism. They should not only know the pressure warehouse, but also need to develop a reasonable inventory and a reasonable pricing mechanism so that the network growth rate can be synchronized with the market growth rate.

Survey: Forecast of domestic auto market trends in the fourth quarter of 2012

2011 was defined as the year in which China's auto market is returning rationally, and it is a watershed that has ended the explosive growth of previous years. At the beginning of this year, the car industry generally predicted that China’s auto market will gradually pick up, but it’s counterproductive. The decline in 2011 apparently did not quickly reverse in 2012. The auto market continued to be tepid in the first two quarters, and it came to a low sales point in July. In contrast, just in the past August, China’s car sales rebounded strongly, with sales of 1.4952 million, an increase of 8.26% year-on-year. among them. Passenger car sales reached 12.189 million units, an increase of 11.3% over the same period of last year. From January to August, passenger car sales increased by nearly 8% year-on-year, basically maintaining the trend of stabilization and recovery.